Sovereign Wealth Funds and Faith in the USD

Posted on 07/13/2011

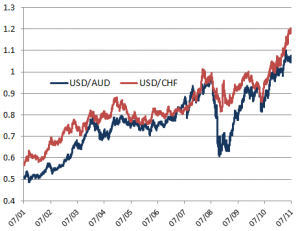

It is true that most sovereign wealth funds and global institutional investors have a high allocation to U.S. dollar-denominated assets. This has been the story for the past half century. Second, it has been a difficult time for the U.S. dollar this past decade. With the bailout of financial institutions, mounting federal and state governmental […]